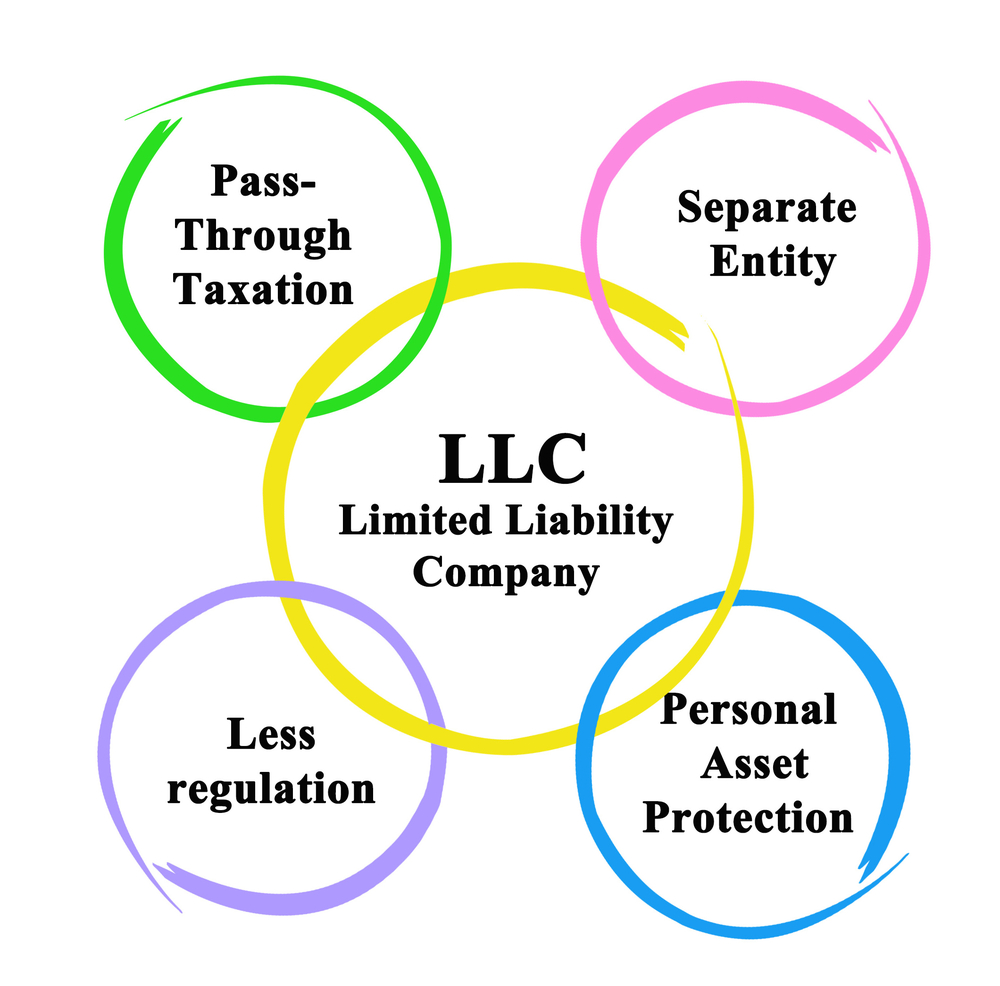

A limited liability company (LLC) is a legal business entity that offers certain liability protection (like a corporation) and other features similar to a partnership.

The owners of an LLC are called members, and LLCs can have several different types of owners, including some other types of businesses.

A single-member LLC may be owned by a corporation or a partnership, and foreign LLCs (those formed under the laws of another state) may have different requirements for LLC membership. Some states require members of an LLC to identify themselves in the registration document, while other states do not.

A company that is formed as a professional LLC (PLLC) is restricted as to the types of owners it can have, and some states do not allow PLLCs, Generally, only certain licensed professionals, such as doctors, lawyers or accountants, may form PLLCs. However, states differ in the types of professionals they allow as members of the LLC.

Generally, members must be identified and their professional licenses must be examined and approved when the company is formed. LLC members have limited liability for the debts, obligations and liabilities of the business.

Limited liability does not mean that the owners of the business have total immunity from any liability. It only means that the individual member's liability is limited to his or her investment in the business.

LLC members have personal liability if they have personally guaranteed loans or other debts or if they act outside the limits of their obligations to the business. For example, limited liability cannot protect a member who steals from the business or harasses someone. have personal liability if they have personally guaranteed loans or other debts or if they act outside the limits of their obligations to the business. For example, limited liability cannot protect a member who steals from the business or harasses someone.

As with any other type of business, there must be someone in charge of the LLC for day-to-day and long-term decisions.

Members can choose to manage the LLC themselves, or they can appoint or hire a manager or managers.

The management of the LLC is usually spelled out in the application to the state and also in the LLC operating agreement. Whoever has managerial responsibility for the LLC's finances and operations has general (not limited) liability for its management decisions and actions.

If the members decide to manage the LLC themselves, they can set up the management in any way they wish.

A formal board structure is not required, but it is a good idea for the members of the LLC to meet formally at least once a year and to keep records of the decisions they make at their meetings.

A multi-member LLC is taxed as a partnership, so each member's share of net income or loss is carried forward on the member's personal tax return. In a multi-member LLC, the operating agreement determines each member's share of the company's liabilities and of the company's profits and losses.

An LLC may also elect to be taxed as a corporation or an S corporation, and then the members would be taxed in the same manner as shareholders of a corporation or owners of an S corporation.

LLC members who are individuals are considered self-employed and not employees. They must pay self-employment tax on their share of the net income of the business.

When an LLC is formed, it can decide who can become a member (owner) of the company, but it must conform to state and federal laws.

States differ in their requirements for LLC ownership. The requirements for ownership of a specific LLC must be spelled out in the company's operating agreement. Professional LLCs (PLLCs) are a special case. States that permit PLLCs restrict ownership to certain types of professionals.

Some states do not have a PLLC business type, but allow licensed professionals to form a regular LLC. Illinois, for example, allows firms to form a standard LLC for professional services if all members are licensed.

A firm can buy another firm and keep the firm's previous legal form. If an LLC is owned by another company, it is usually formed as a subsidiary of the parent company, which is usually a corporation.

The parent company owns and controls the subsidiary (the LLC). A parent company may have several LLCs for different purposes.

In real estate, for example, a corporation may own several LLCs, each with different properties, to separate the liability of one from the other.

The Supreme Court (in United States v. Bestfoods) said that a parent company is not liable for the acts of its subsidiaries.

The managers of an LLC do not usually have titles such as CEO, and an LLC does not have a board of directors like a corporation. However, some members of an LLC do have titles, depending on whether or not they participate in the management of the company.

LLCs can be managed by a member or by a non-member.

The non-member manager is usually a professional manager or a management organization.

In some cases, a group of LLC members may manage the business. A single member managing an LLC may be called a member-manager or member-manager.

The term articles of incorporation is used by most states, but your state may refer to the document by another name, such as a certificate of formation.

For income tax purposes, a single-member LLC is treated as an entity separate from its owner, unless you file Form 8832 and elect to be treated as a corporation.

Although the information required varies from state to state, you will generally only need to provide the name and address of your LLC and the names of its members.

Filing this form ensures that the name will be available as you move through the other steps of forming an LLC.

If your state has a publication requirement, check with your state's secretary of state office for more information on the content of the notice, how many times it must be published, and any other requirements that may apply.

Whether you are new to the world of business formation or have been through this process before, it is easy to get bogged down in the details, laws, and requirements to get your idea off the ground.